At Alummira, our sole focus is decoding the rhythm of aluminum—the sharp ascents, the jarring corrections, and the quiet signals in between. The month of April 2026 provided the most dramatic canvas for our work since the company was founded. It was a month that saw global aluminum prices surge to near-historic peaks on a cascade of supply catastrophes, only to retreat as the gravitational pull of regional imbalances and monetary policy reasserted itself. What follows is Alummira’s chronological reconstruction of that extraordinary month, dissecting the forces that drove prices up and then pulled them back down, and extracting the lessons that will define the market for years to come.

The Opening Tremors: A Market Already on Edge

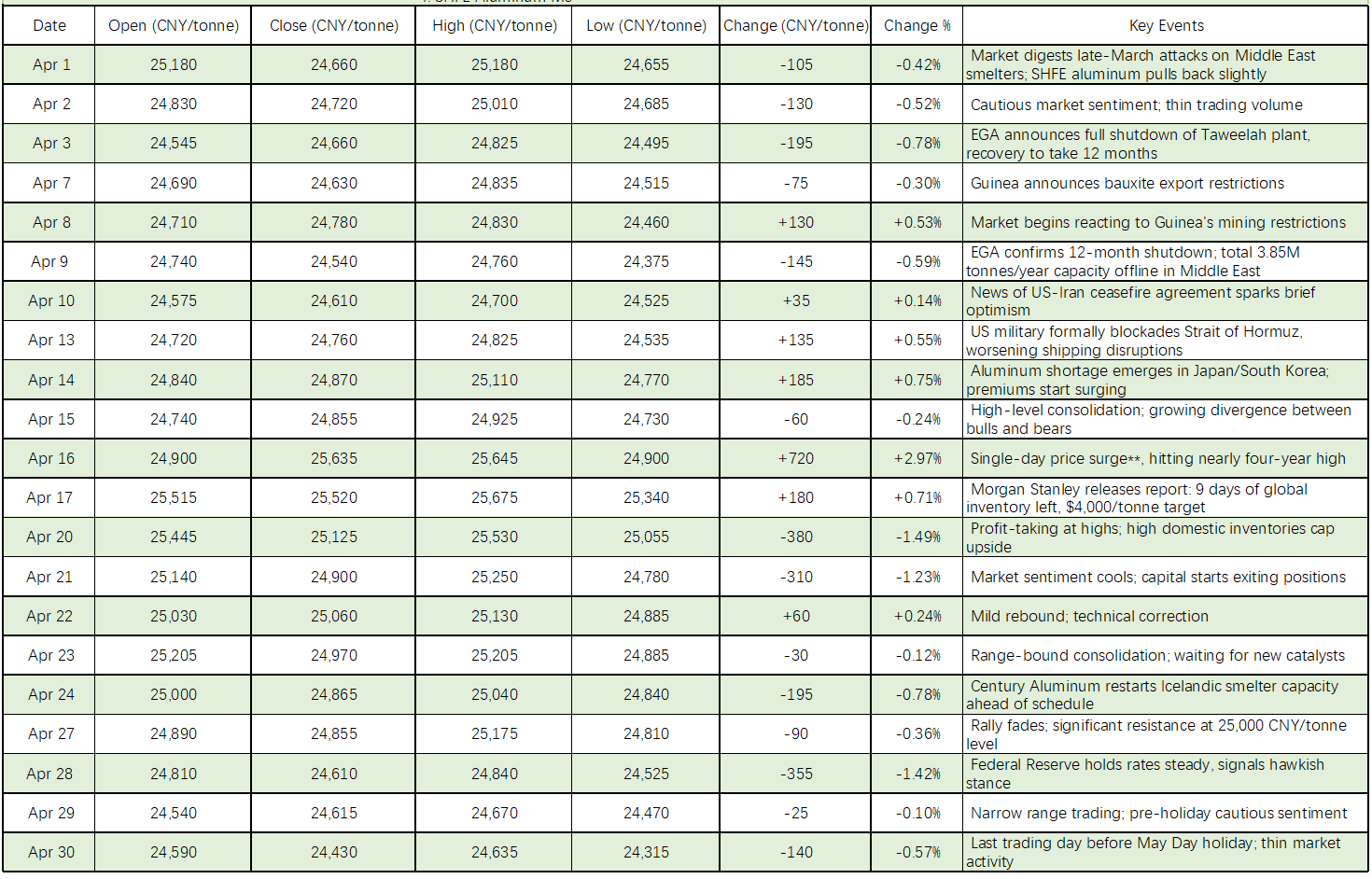

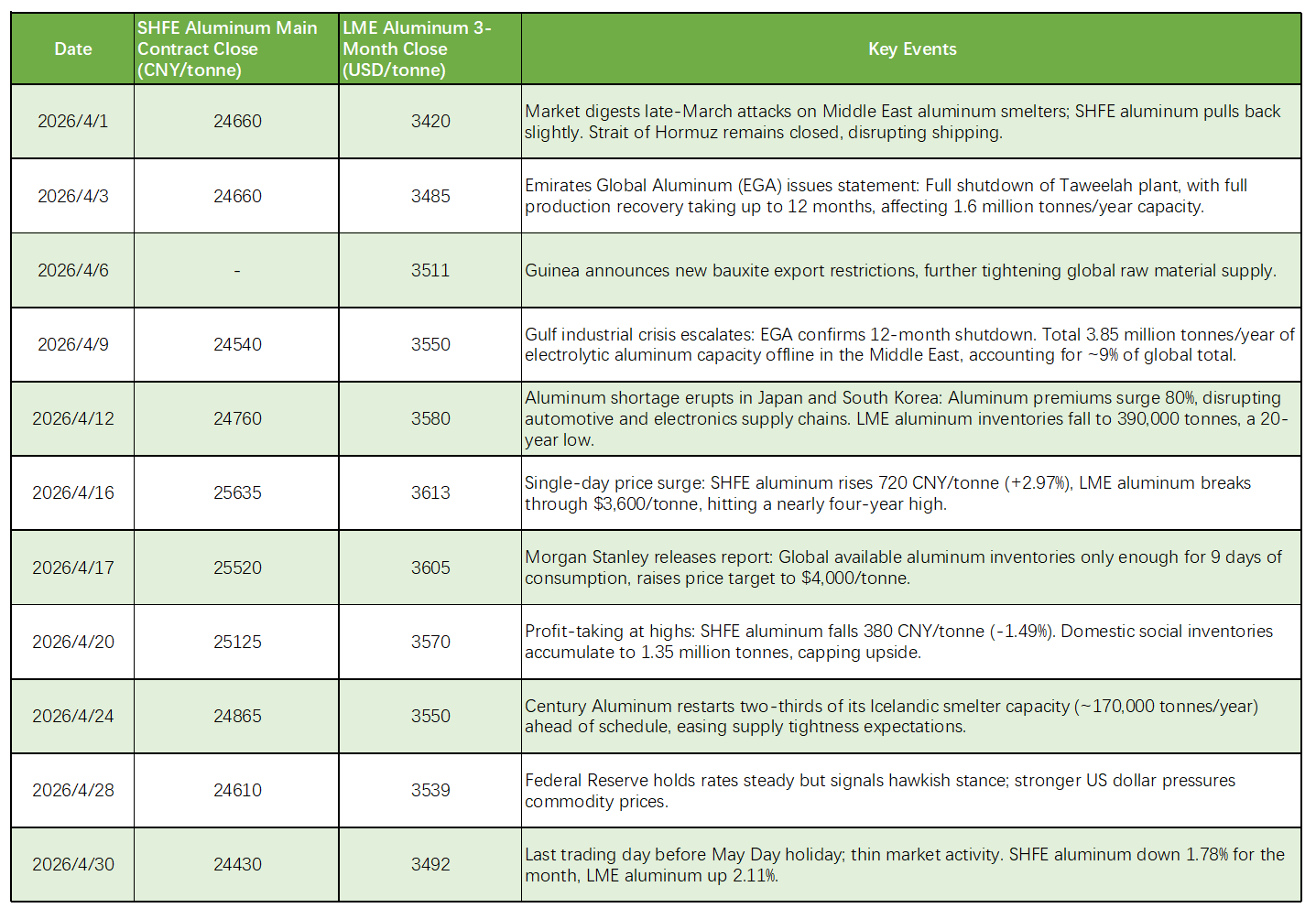

When trading desks flickered to life on April 1, the aluminum market was anything but calm. The SHFE front-month aluminum contract settled at 24,660 yuan per tonne, while the three-month LME benchmark stood at $3,420 per tonne. The Strait of Hormuz, a lifeline for global alloy shipments, remained closed following the late-March attack on a major Middle Eastern smelter. Alummira’s early-warning indicators were already flashing caution: freight disruptions had begun to pile up, and physical traders were quietly scrambling for units. The price action was tentative, a small step down in Shanghai, a modest tick up in London—the market was holding its breath.

The exhalation came on April 3, and it was a gasp. Emirates Global Aluminium (EGA) released an operational bulletin that Alummira analysts immediately flagged as a tectonic event. The Taweelah smelter complex, representing 1.6 million tonnes of annual electrolytic capacity, had suffered total operational paralysis. The official timeline for a full recovery was pegged at up to 12 months. In an instant, a volume equivalent to roughly 2% of global primary aluminum production was removed from the chessboard. The Alummira pricing model began recalibrating its scarcity projections overnight.

The Perfect Storm Assembles: Guinea and the Gulf Inferno

If the EGA news lit the fuse, the events of the following week packed the explosives. On April 6, Guinea, which feeds approximately 40% of the world’s seaborne bauxite, announced a new set of raw material export restrictions. Bauxite, the ore that feeds alumina refineries and ultimately smelters, was suddenly being choked at its source. Alummira’s raw-material stress index spiked to levels not seen since the Indonesian export bans of the previous decade. The upstream pressure was now being applied simultaneously with the downstream smelting crisis, a rare double squeeze.

Then came April 9, the day the Gulf situation escalated from an isolated incident into what Alummira’s geopolitical risk assessment termed an “industrial-scale supply war.” The full scope of the outage became clear: EGA’s 1.6 million tonnes, Alba’s 308,400 tonnes, and Qatalum’s 650,000 tonnes—a combined 3.85 million tonnes of electrolytic capacity, representing 9% of the global total, was abruptly idled. Alummira’s head of research circulated an internal memo with a stark title: The Missing Ninth—A Permanent Scar? The question of permanence would linger over every subsequent price move.

Inventory Abyss and the Panic in Asia

The physical market began to scream what the futures market was still only murmuring. On April 12, Alummira’s premium-tracking desk recorded a historic dislocation in Asia. The benchmark Japanese aluminum premium erupted by 80% to $450 per tonne over LME cash, an all-time record. Korean buyers reported being unable to find spot cargoes for immediate shipment. The automotive and electronics supply chains, heavily reliant on just-in-time aluminum deliveries, were facing the prospect of assembly-line stoppages.

Behind the premium explosion lay a chilling inventory reality. The London Metal Exchange reported that total on-warrant stocks had collapsed to 390,000 tonnes, a two-decade low. More critically, Alummira’s analysis of LME warrant holdings showed that non-Russian material available for delivery had dwindled to less than 150,000 tonnes. For an industry that consumes roughly 190,000 tonnes per day globally, the arithmetic was terrifying. The Alummira supply-cushion monitor, which tracks days of consumption cover, was printing readings below ten days for the first time in the company’s history.

The Vertical Ascent: April 16 and the New Peaks

What happened on April 16 could only be described as a vertical price event, and Alummira’s trading screens that afternoon were a blur of green. The SHFE aluminum price rocketed by 720 yuan per tonne, an intraday gain of 2.97%, to close at 25,635 yuan. On the LME, the three-month contract crashed through the $3,600 barrier to settle at $3,613 per tonne, a level not seen in nearly four years. Alummira’s breakout-alert system triggered three times during the session, a frequency normally associated with extraordinary market dislocations.

The following day, April 17, Morgan Stanley lent institutional weight to the firestorm, publishing a report that explicitly targeted $4,000 per tonne for aluminum. The bank calculated that global available inventory was down to just nine days of consumption. Within Alummira’s morning strategy call, the debate was not about whether the number was accurate — our own data essentially confirmed it — but about whether the market was adequately pricing the probability of additional supply losses. As the Shanghai price touched 25,520 yuan and London held above $3,600, a palpable sense of euphoria settled over the bull camp. This, it seemed, was the dawn of the super-cycle.

The Recoil: High Inventories and a Hard Landing in Shanghai

It is often said that the market’s most instructive moves are not the surges but the reversals, and Alummira’s analytical framework places particular emphasis on identifying the turning points. On April 20, the first crack appeared, and it came from Shanghai. The SHFE aluminum price slumped 380 yuan (-1.49%) to 25,125 yuan in a single brutal session. The catalyst, which Alummira’s China desk had been increasingly vocal about, was the domestic inventory overhang. Social inventories of primary aluminum ingots across China’s eight major consumption regions had swelled to 1.35 million tonnes. This domestic stockpile, though partially structural given China’s role as the world’s swing producer, acted as a powerful restraint on Shanghai’s ability to follow London into a full-blown crisis rally. The Alummira price-deviation indicator, which measures the divergence between SHFE and LME, was sounding a loud warning: this was not one global market, but two, moving increasingly to their own beats.

Additional relief came from an unexpected quarter. On April 24, Century Aluminum announced the early restart of two-thirds of its curtailed capacity at its Grundartangi smelter in Iceland, adding roughly 170,000 tonnes per year back to the Atlantic basin. While a modest volume against the 3.85 million tonnes lost in the Middle East, the restart served as a psychological circuit breaker. Alummira’s flow-of-funds tracker observed a noticeable reduction in speculative long positioning on the LME in the following sessions, as momentum-driven traders reassessed the case for an uninterrupted climb.

The final anchor dragging prices lower was the macro environment. On April 28, the Federal Reserve held rates steady but accompanied its decision with decidedly hawkish language, insisting the inflation battle was unfinished. The dollar surged, and with it, the cost of holding dollar-denominated aluminum for non-U.S. buyers increased. The LME three-month price retreated to $3,492 by month-end. Alummira’s correlation matrix, which tracks the interplay between the dollar index and aluminum, flashed a classic inverse move, reminding the market that no commodity exists entirely on its own fundamentals.

A Tale of Two Benchmarks: April 30 Closes

As traders squared their books on April 30, the final session before China’s extended Labor Day holiday, the numbers presented a starkly bifurcated picture. The SHFE main contract settled at 24,430 yuan per tonne, having lost 1.78% over the full month. The LME three-month contract, by contrast, printed $3,492 per tonne, booking a monthly gain of 2.11%.

For Alummira, this divergence encapsulates the entire narrative of April 2026. The crisis was fundamentally a seaborne, ex-China phenomenon. London prices reflected a world suddenly starved of Middle Eastern units, facing a logistics blockade, and staring at empty exchange warehouses. Shanghai prices, meanwhile, mirrored a domestic ecosystem operating at over 97% utilization and sitting on a mountain of ingots that, while not infinite, provided a formidable buffer against panic. The two prices told two different stories, and Alummira’s clients who understood this bifurcation were the ones best positioned to navigate the chaos.

The Deeper Currents: Demand Transformation and the Capacity Wall

Beneath the surface-level price gyrations, Alummira’s sectoral demand monitor was capturing a profound structural shift that will far outlast the events of April. The traditional “Silver April” peak in construction and industrial activity was undeniably tepid. China’s property sector continued its secular decline, and photovoltaic installations, while still growing, no longer provided the same marginal acceleration. These headwinds were real, and they were the primary reason Shanghai prices failed to join London’s parabola.

However, Alummira’s forward-looking indictors were beginning to trace a new demand architecture. The electric vehicle supply chain, with its insatiable appetite for lightweight aluminum body panels, battery trays, and thermal management components, was scaling new highs. The global buildout of AI computing infrastructure was emerging as a massive new demand sink, consuming high-spec aluminum for data center racking, busbars, and power cabling. Grid investments, driven by the renewable energy transition, and the accelerating substitution of aluminum for copper in electrical applications added further layers of structural demand growth. In China specifically, this new demand constellation was running directly into a regulatory ceiling: domestically, operational capacity had reached the government-mandated limit of 45 million tonnes, with utilization rates structurally above 97%. There was simply no more supply-side elasticity to tap.

The Alummira Outlook: From Mirage to Permanent Reality

As we at Alummira survey the landscape from the vantage point of late April 2026, our analytical conviction has only strengthened. The April event was not a speculative episode destined to fully unwind; it was a preview of a permanent scarcity environment. The capacity lost in the Middle East—some of it, as assessments indicate, irreversibly damaged—will not seamlessly return. The logistical premium introduced by the Hormuz closure and the resource nationalism signaled by Guinea have translated into a structural cost elevation that is unlikely to dissipate quickly.

For the short term, we anticipate a period of high-level consolidation. Our Alummira SHFE forecast models a range of 24,500 to 26,000 yuan per tonne for the coming months, driven by the tug-of-war between high domestic inventories and the gravitational pull of global tightness. For the LME, we see a wider oscillation between 3,300 and 3,300 and 3,800 per tonne, with persistent upside risks triggered by any incremental draw in exchange inventories.

Looking further out into the second half of 2026 and beyond, Alummira’s base case is unambiguous: a widening physical deficit will drive a sustained uplift in the price floor. The $4,000 per tonne target on the LME, which appeared briefly as a speculative zenith in April, has now metastasized into a fundamental destination. In Shanghai, the combination of a rigid capacity ceiling and an expanding new-demand base makes a push toward and beyond 27,000 yuan per tonne a matter of time, not possibility.

At Alummira, our name has always reflected our mission: to illuminate the cycles of the aluminum market, from their shimmering peaks to their troughs of despair. April 2026 was a month that tested every participant, and it will stand as a defining chapter in our ongoing chronicle of this essential industrial metal. The message we take from it is clear: the era of abundant, geopolitically serene, and logistically frictionless aluminum supply has ended. In its place, a new, harder, and structurally higher-priced reality has begun to take shape. Alummira will be here, as we have always been, to chart every swing along the way.